Power needs power: electrical, computing and cell power are the bricks of the digital prison

Deja vu: building the 15-min-city digital ghetto in the same pattern of the COVID prison.

Context

Depopulation or extermination?

This research took 113 hours (including late night work), that will save you that amount of reading and organizing ideas. If you like it, please consider a paid subscription:

The real COVID timeline

Search engines are detecting “covid-19” years before the PLANdemic, but don’t show the sources. Could you please help with advanced searches by limiting the term (also covid19) to prior years? (add links as comments, think this as a truth wiki)

The PLAN revealed

This research took many many hours (including late night work), that will save you that amount of reading and organizing ideas. If you like it, please consider a paid subscription:

2030 AI industry (USA)

https://ig.ft.com/ai-data-centres/

Total computing power: 100 million H100e

It’s the peak or effective computing power of the installed cluster, not something accumulated or produced over a year.

H100-equivalents means the number equivalent of NVIDIA H100 GPUs, so 100 million H100e means 100,000,000 units of such computing hardware ≈ 100 exaFLOPS.

100 million H100 are from 3x to 10x of the effective tensor compute of the entire US PC fleet (300 million desktops and laptops). Or vice versa, the PC fleet is from 10% to 30% of the AI projected computing power.

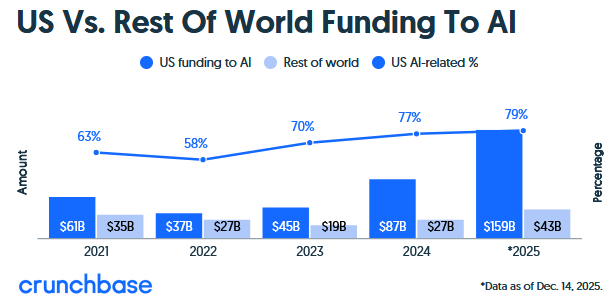

Total investments: $ 2000 billion USD

$ 4000 billion in AI investments worldwide.

In April 2025 McKinsey predicted that $ 5200 billion of investment in data centers would be required by 2030.

SpaceX was a covert NASA/DoD incubated incubus, despite the initial investments of Google and Fidelity ($1 billion, 2015) followed by Founders Fund and Andreessen Horowitz ($1.9 billion, 2020):

Just as with Starlink being unviable without the billion dollar government contracts, there’s no way that market income could repay AI investments in the trillions of dollars, proving that they are just building the excess computing power for our digital cage:

Resistance to Paying: Consumer willingness to pay remains a significant hurdle; for example, 50% of U.S. smartphone owners refuse to pay extra for AI features. Many subscribers are already feeling “subscription fatigue,” with 54% viewing current AI pricing models as a “rip-off”.

Paying Users: 2 billion consumers use AI tools globally but only 3% (roughly 54 million) currently pay for premium subscriptions.

OpenAI (ChatGPT Plus/Pro): 11 million paying subscribers as of December 2025, making it the market leader ~800 million weekly active users (including free tier).

Google (Gemini): ~650 million monthly active users as of November 2025 (mostly free tier, paid users in the low millions). Paid retention is reportedly lower than competitors, with ~60% of subscribers still active after six months.

Anthropic (Claude Pro/Max): 30 million monthly active users overall as of Q2 2025, but paid subscribers in the single-digit millions, focused more on enterprise.

Other Services: Microsoft Copilot Pro and Midjourney add several million more paid users combined, with Midjourney alone generating $200 million in annual recurring revenue (ARR) from ~1-2 million subscribers at $10-60/month.

Total US AI revenue hit ~$41 billion in 2025, part of a global market exceeding $70 billion.

Compare that income with 2025 investments:

Corporate Capex: Hyperscalers spent $443 billion in 2025 (projected $602 billion in 2026), 75-80% on AI. Breakdown: Microsoft ($80B), Meta ($60-65B), Amazon/Google similar.

Venture Capital: $202 billion total in AI (infrastructure, labs, apps), with 58% in $500M+ rounds. Examples: OpenAI ($40B), Anthropic ($13B), xAI ($10B). AI startups raised a record $150 billion globally (79% in the US)

Military Contracts: Defense tech startups raised $19 billion overall. Military is ~5-10% of total funding. DoD awarded $200 million each to Anthropic, Google, OpenAI, and xAI in July 2025 for AI workflows. Total DoD AI funding: $1.8-2.5 billion FY2025.

Total electric power: 120 GW (1 PetaWh)

Power consumption is a proxy to computing power.

Rule of thumb 1 GW ≈ 1 million H100-equivalents.

Training a new model requires vast amounts of new calculations and power:

120 GW of continuous average power draw equates to ~1,051 TWh (terawatt-hours ~ 1 trillion Wh ~ 10¹²) of electricity consumption per year (calculated as 120 GW × 8,760 hours/year = 1,051,200 GWh).

This is a massive amount—25% of total U.S. electricity consumption in 2024 (~4,100–4,200 TWh).

Cities: Equivalent to the combined annual electricity use of the 30 largest US cities. The highest-consuming cities “only” use 50 TWh/year (e.g., Houston ~45–50 TWh, New York City ~50–55 TWh).

States:

Roughly matches California (~250–270 TWh/year) + Florida (~250 TWh) + New York (~150 TWh) + Pennsylvania (~140–150 TWh) + several mid-sized states.

Equivalent to all Northeast states combined (New England + Mid-Atlantic, ~400–500 TWh total).

The combined consumption of the 15 smallest states (e.g., Vermont ~5–6 TWh, Wyoming ~15 TWh, etc.).

States:

2x Texas (the highest-consuming state at ~500–525 TWh/year).

4x California.

7x New York.

Regions:

Comparable to the electricity of the entire Midwest region (~800–1,000 TWh across multiple states) or significant portions of the Southeast/South.

This scale highlights why projected AI data center growth (often discussed in tens to hundreds of GW) poses major grid challenges.

Most rely on natural gas. All four hyperscalers have struck landmark deals for nuclear power in 2024. Microsoft is restarting the Three Mile Island nuclear plant (famous for the nuclear accident).

When gas is gone, only nuclear power will be able to power the AI monster.

The landrush for electrical power

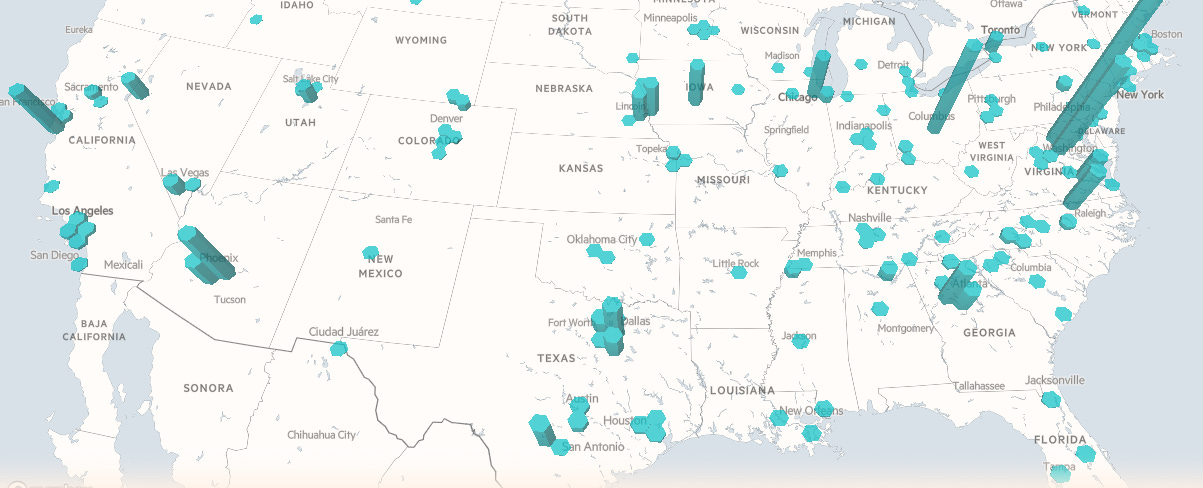

1 second glimpse: data centers are popping up like mushrooms

2025. Height indicates aggregate IT load:

AI energy report:

Grok update:

$525 billion Stargate: 7 M H100e, 10 GW

Stargate = OpenAI, Oracle & SoftBank

Stargate, Abilene, TX (and expansions): 7 GW total planned (projected phased rollout with initial 1 GW by mid-2026, scaling through 2027-2028) Estimated computing power: ~7 million H100-equivalents / ~7–14 exaFLOPS Estimated total investment: $400–500 billion (tied to nearly 7 GW capacity and full $500 billion commitment for up to 10 GW by 2029)

$25 billion Vantage buyout by SoftBank:

SoftBank/Stargate announced plans to acquire the owner, DigitalBridge, by 2026.

The company operates across North America, EMEA, and Asia-Pacific, with over 35 campuses and more than 2.6 GW of capacity (operational or planned).

Frontier Texas, Shackelford County, TX: 1.4 GW (projected by 2028) Estimated computing power: ~1.4 million H100-equivalents / ~1.4–2.8 exaFLOPS Estimated total investment: $25 billion (announced for full Frontier campus development)

$108 billion Amazon

Canton Campus, Canton, MS: 0.8 GW (projected by late-2026)

Ridgeland Campus, Ridgeland, MS: 1 GW (projected by late-2027)

Pennsylvania AI Innovation Campuses, Salem & Falls Townships, PA: Capacity not announced (projected ongoing/permitting as of 2026)

NC Campuses, Multiple counties (e.g., Richmond County), NC: Capacity not announced (projected full build-out by 2027-2028)

Sunbury Campus, Sunbury, OH: Capacity not announced (projected completion by 2034) Estimated computing power: ~1.8 million H100-equivalents / ~1.8–3.6 exaFLOPS Estimated total investment: $40–50 billion (part of $100+ billion 2025 CapEx; includes Mississippi, Pennsylvania, and other state projects)

$15 billion Anthropic & Amazon: 1.2 M H100e

Project Rainier, New Carlisle, IN: 1.2 GW (projected operational scaling through 2026) Estimated computing power: ~1.2 million H100-equivalents / ~1.2–2.4 exaFLOPS Estimated total investment: $11–15 billion (includes $11 billion Rainier campus and $8 billion partnership)

$100 billion Meta: 6 M H100e, 6 GW

Prometheus, New Albany, OH: 1 GW (projected by mid-2026)

Hyperion, Richland Parish, LA: Estimated computing power: ~6 million H100-equivalents / ~6–12 exaFLOPS Estimated total investment: $60–100 billion (hundreds of billions pledged for multi-GW titan clusters; includes Hyperion JV and broader AI CapEx ramp):

Three new combined-cycle natural gas turbines totaling 2.26–2.3 GW capacity: 2 in Richland Parish (online late-2028), 1 at an existing site (online 2029).

Up to 1.5 GW of new solar resources (expedited procurement, to offset gas reliance and support Meta’s clean energy matching goals).

Extensive transmission upgrades: ~100 miles of 500kV lines, eight new 230kV lines, multiple substations (including customer-owned ones).

$80 billion Microsoft: 6 M H100e, 6 GW

Fairwater (multi-site, primarily Mount Pleasant, WI): ~5 GW aggregate (projected by late-2027; includes phased expansions)

Fayetteville (location AR/NC): 1 GW (projected by early-2026)

Mount Pleasant, Racine County, WI: Capacity not announced (projected phase 1 by early-2026) Estimated computing power: ~6 million H100-equivalents / ~6–12 exaFLOPS Estimated total investment: $50–80 billion (part of $80 billion 2025 AI commitment; includes $7.3 billion Wisconsin phases)

$75 billion Google DeepMind: 4 M H100e, 4 GW

New Albany Campus, New Albany, OH: 0.7 GW (projected by mid-2026)

Omaha Campus, Omaha, NE: 0.5 GW (projected by mid-2027)

Pryor Campus, Pryor, OK: 0.3 GW (projected by mid-2026; based on phased expansions)

Fort Wayne Campus, Fort Wayne, IN: Capacity not announced (projected ongoing as of 2026) Estimated computing power: ~1.5 million H100-equivalents / ~1.5–3 exaFLOPS Estimated total investment: $15–20 billion (includes $9 billion Oklahoma expansions; part of broader $75+ billion AI CapEx)

$15 billion Crusoe. Tenant: Google. Goodnight, TX: 0.9 GW (projected by mid-2027) Estimated computing power: ~900,000 H100-equivalents / ~0.9–1.8 exaFLOPS Estimated total investment: $10–15 billion (multibillion-dollar pipeline; includes Abilene/Goodnight phases)

$40 billion xAI: 2 M H100e, 2GW

Colossus 2 (and expansions), Memphis, TN: 2 GW (projected by early-mid 2026; including third building acquisition) Estimated computing power: ~2 million H100-equivalents / ~2–4 exaFLOPS Estimated total investment: $30–40 billion (tens of billions for GPU-heavy expansions to 1-2 million chips)

$3 billion CoreWeave: 1 M H100e, 1 GW

Helios, Afton, TX: 0.8 GW (projected by 2029) Estimated computing power: ~800,000 H100-equivalents / ~0.8–1.6 exaFLOPS Estimated total investment: $2–3 billion (includes $1.4 billion financing for Helios phases)

Tenants: revenue backlog (over $55 billion as of late 2025)

OpenAI — Largest direct client with contracts totaling ~$22.4 billion (initial $11.9B in March 2025, expanded by $4B and then $6.5B).

Microsoft — Long-standing anchor customer (historically ~62% of revenue in 2024; concentration reduced to <35% by late 2025).

Meta — Multi-year expansion worth $14.2 billion.

Others — Nvidia, Alphabet (Google), IBM, Cohere, CrowdStrike, Poolside, Rakuten, Jasper, Goldman Sachs, Morgan Stanley, and various AI startups/labs (acquisition of Weights & Biases added ~1,400 enterprises)

Other:

Cologix Johnstown, Johnstown, OH: 0.8 GW

Compass Meridian Campus, Lauderdale County, MS: 0.3 GW (projected by 2033)

Note: why isn’t Microsoft listed in Stargate

Evolution of the “Stargate” Name and Structure The original “Stargate” concept (reported in 2024) was a proposed ~$100 billion AI supercomputer project directly between Microsoft and OpenAI (as Phase 5 of their long-term partnership), potentially needing up to 5 GW and launching around 2028. That was essentially Microsoft financing and hosting massive dedicated capacity for OpenAI on Azure.

2025 Reboot as a New Venture By January 2025, “Stargate” was relaunched as Stargate LLC — a standalone multinational joint venture announced at the White House. The core equity partners/funders became OpenAI, SoftBank, Oracle, and MGX (Abu Dhabi’s investment arm).

SoftBank handles primary financial responsibility.

OpenAI has operational control.

Oracle leads much of the actual data center build-out (e.g., the flagship Abilene, TX site and the 4.5 GW+ expansions). This shift allowed OpenAI to diversify away from heavy reliance on Microsoft’s Azure for future massive-scale training, amid growing compute demands and some reported tensions in the partnership.

Microsoft’s Role in the New Stargate Microsoft is explicitly listed as one of the “key initial technology partners” (alongside NVIDIA, Arm, and Oracle). This means Microsoft continues providing cloud services, IP access, and integration support — including for some Stargate-related workloads — but does not contribute equity capital or directly own/build the Stargate campuses.

Their existing partnership (dating back to 2019, with Microsoft having invested ~$13–14 billion total) remains intact through 2030, with revenue sharing, Azure exclusivity for certain APIs, and a “right of first refusal” on new capacity.

OpenAI still uses Azure heavily (and committed to more in 2025), but Stargate represents a parallel, diversified path for hyperscale infrastructure.

In short: Microsoft’s massive prior investment in OpenAI (which powers much of ChatGPT today) and shared infrastructure history influenced the original Stargate idea, but the 2025 version is structured as OpenAI’s push for independence in infrastructure ownership — with Microsoft staying as a key collaborator rather than a consortium co-leader.

Amazon and Google are similar cases to Microsoft, proving they are all a monopoly disguised as competition.

Military

No publicly available data exists on projected electrical capacities (in GW or MW scale) for dedicated US military AI data centers as of early 2026.

Due to national security concerns, military and intelligence community facilities (e.g., those operated by the NSA, DISA, or DoD) remain highly classified even for power requirements, especially for AI-specific workloads:

NSA Utah Data Center (Bluffdale, UT, operational since ~2014) → Designed for massive data storage and processing (intelligence/surveillance). It features a power capacity of 65 MW (enough for ~65,000 homes). No public updates tie this directly to modern AI training/inference, and no projections for expansions exist in open reports.

DISA Defense Enterprise Computing Centers (DECCs) → DISA manages multiple core data centers (e.g., in Mechanicsburg, PA, and others CONUS/OCONUS). Recent efforts focus on modernization (e.g., a 2025 $931M contract with HPE for hybrid cloud/AI-enabled infrastructure), but no specific power capacities or AI-dedicated projections are disclosed.

The DoD increasingly uses commercial cloud providers (e.g., via JWCC contracts with AWS, Microsoft Azure, Google Cloud, Oracle) for AI workloads, rather than building standalone hyperscale AI facilities. This shifts much of the power burden to private-sector data centers.

Recent initiatives (e.g., Air Force offering unused base land for private AI data centers requiring >100 MW each) suggest partnerships with industry, but these are not purely military-owned/operated.

Due to the masonic concept of rigged public-private partnerships, the DoD is funding part of the AI surge but most comes from the private sector.

“National Security” stamps out all City/County, State and Federal regulations. This means that military appropriation of private land is equivalent to the Chinese Communist Party not following any regulation when building their AI centers. So to defeat the unfair competition of Chinese lack of red tape, the US government just turns private land into military use and gives it to the private sector, happy to avoid the costs of all regulations: construction, environmental, social, noise, electrical, nuclear, depleting the power grid (blackouts, especially when training a new model, which creates a power surge), etc.

Notice the “nuclear” word? The lack of nuclear control could lead to a nuclear disaster, which will be “confidential” if it happened on military land.

The lack of any control also leads to cut vast forest or farm areas to deploy solar panels just because hyperscalers like Meta wants to “green” it’s energy matrix by killing/replacing natural green with artificial green.

Note: there’s no such thing as “green energy”, since all “clean” “green” tech causes environmental damage, most of the times, even worse than conventional energy, especially in the case of gas and hydroelectric. It’s as if Meta would be painting farmland with toxic green paint killing the green vegetation, under the excuse of greening!

This comment is very important:

“I worked for the Bureau of Land Management for years as a Geologist in a field office in Wyoming. I have seen original documentation setting aside areas specifically for “Military Reservations” - yes, that’s the terminology. So, not only land patents but also the initial reservation of these lands specifically for military purposes, such as the Executive Orders doing so.

We have gone so far down the road - the opposite direction of the Constitution - of government joining up with private business, that “public-private partnerships” are everywhere, and in virtually every aspect of our lives. It sounds like this BS will / is being used as an excuse for private companies to “use” miliary reservation lands for “military purposes.” However, we should all know that that is just an excuse to join military with private corporate interests. And, that that really only serves one master - private corporate interests. Which serves as further evidence that our government and military have been almost completely captured by private corporate interests - and thus, that General Smedley Butler’s experience is still occurring, and is fast approaching total consumption / absorption of “our” government and military.”

Watch the water

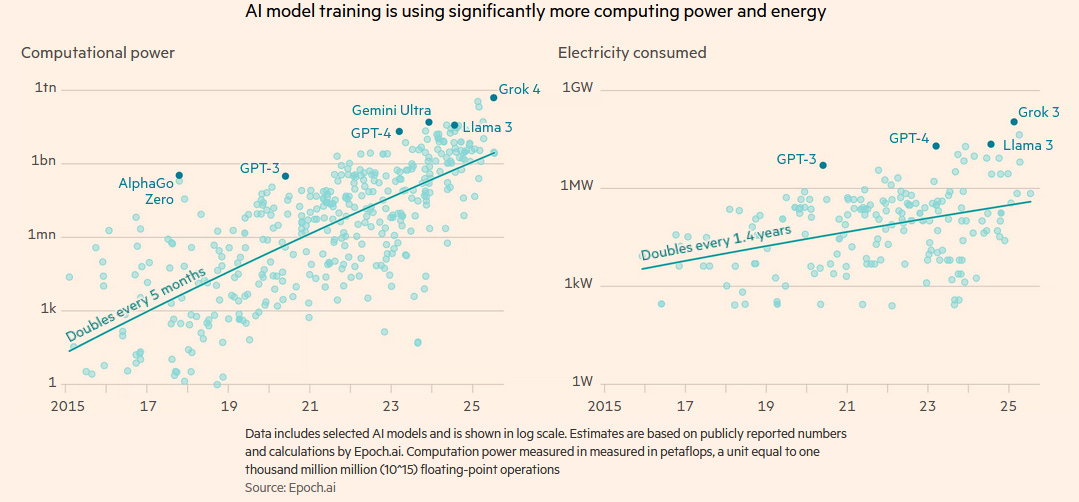

FT. “OpenAI’s Sam Altman has said he envisages facilities that will go “way beyond” 10GW of power, requiring “new technologies and new construction”.

They believe in an endless “AI scaling law”: more data and more computing power will deliver more intelligence.

Nvidia said in May 2025 that Big Tech companies were adding tens of thousands of its latest GPUs to their systems every week, a pace that was only set to accelerate as its next-generation “Blackwell Ultra” systems were rolled out. The chipmaker’s roadmap projects that in 2027, its “Rubin Ultra” systems will cram more than 500 GPUs into a single rack that will consume 600 kilowatts of power, creating fresh challenges on energy and cooling.

Cooling requirements are growing more complex after Nvidia said that its latest Blackwell chips would require direct-to-chip cooling, where coolant is passed through metal plates that are attached to GPUs, CPUs and other heat-generating components, just as water passess through the radiator of a car.

The US consumed 55 billion liters of water in 2023. Indirect consumption tied to energy use is markedly higher at 800 billion liters a year, the equivalent annual water usage of almost 2 million homes.

The heated water is then directed to large cooling towers that use evaporation to reduce the facility’s temperature to a safe range. This leads to huge water loss: 19,000 litres per minute per tower.

Microsoft and others have adopted a closed-loop system that depends on chillers — in effect, a refrigerator —to cool the water”, yet this process is implies more energy.

Another alternative is recirculating sea water.

Conclusion

Interestingly, no globalist climate-action think tank even mentions the energy crisis created by the AI hyperscalers. Just as those billionaires keep using their private jets to attend those conferences, and even promote their power-depleting crypto scam, they won’t even discuss their hypocrisy with respect to AI power suck.

The fact that such a huge computing capacity is underutilized to that extent proves that it’s more than a fad or bubble: they plan to use that capacity to:

track us in their internet of bodies:

https://www.bitchute.com/video/pFvpnftcGpFw/cage us with their internet of things

dominate and persecute us through their AI omnipresent and omnisentient surveillance

Sources

https://empirixpartners.com/the-trillion-dollar-horizon/

https://blog.implan.com/ai-investments

https://www.usfunds.com/resource/ai-data-center-building-spree-hits-40-billion-in-a-single-month/

https://iot-analytics.com/data-center-infrastructure-market/

https://hai.stanford.edu/ai-index/2025-ai-index-report/economy

https://www.goldmansachs.com/insights/articles/why-ai-companies-may-invest-more-than-500-billion-in-2026

https://www.goldmansachs.com/pdfs/insights/goldman-sachs-research/ai-in-a-bubble/report.pdf

https://www.pepperfoster.com/insights/the-artificial-intelligence-ai-roi-report/

https://www.usfunds.com/resource/ai-data-center-building-spree-hits-40-billion-in-a-single-month/

https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/on-the-minds-of-investors/is-ai-already-driving-us-growth/

https://ig.ft.com/ai-data-centres/

https://www-file.huawei.com/-/media/corp2020/pdf/giv/industry-reports/computing_2030_en.pdf

https://www.goldmansachs.com/pdfs/insights/pages/generational-growth-ai-data-centers-and-the-coming-us-power-surge/report.pdf

https://ifp.org/future-of-ai-compute/

https://www.grandviewresearch.com/industry-analysis/artificial-intelligence-ai-inference-market-report

https://www.edge-ai-vision.com/2025/05/ai-chips-for-data-center-and-cloud-to-exceed-400-billion-by-2030/

https://www.eesi.org/articles/view/data-center-energy-needs-are-upending-power-grids-and-threatening-the-climate

https://www.deloitte.com/us/en/insights/industry/power-and-utilities/data-center-infrastructure-artificial-intelligence.html

https://www.rand.org/pubs/research_reports/RRA3572-1.html

https://www.socomec.us/en-us/solutions/business/data-centers/understanding-power-consumption-data-centers

https://www.gartner.com/en/newsroom/press-releases/2025-11-17-gartner-says-electricity-demand-for-data-centers-to-grow-16-percent-in-2025-and-double-by-2030

https://energyanalytics.org/the-rise-of-ai-a-reality-check-on-energy-and-economic-impacts/

https://www.utilitydive.com/news/us-data-center-power-demand-could-reach-106-gw-by-2035-bloombergnef/806972/

9 steps out of global tyranny

Sep 10

Time after time, most have become disappointed with their political leaders, in whom they placed their hopes for change. What they don’t realize is that the root of the problem is the system:

The PLAN revealed

This research took many many hours (including late night work), that will save you that amount of reading and organizing ideas. If you like it, please consider a paid subscription:

Are you prepping?

They are manufacturing a the huge infrastructure and financial crisis !

20 laws we need to exit Extermination Planet

Laws to exit planet prison

No Free Speech without Reach

Why was Bill Gates the mentor of Zuckerberg?

Zuckerberg really flipping?

15 Jan

What Has Happened To Mark Zuckerberg?

How Rumsfeld forced the approval of lethal Aspartame.

Artificial sweeteners, MSG, PFAS, Glyphosate ... go organic!

Why is food poisoning legal?

26 November 2023

This article would be another tool you could share to keep waking-up the still-trusting sleepwalkers: some reject discussing injections, but they’d be open to food.

Solutions for “this” Democracy?

Rethinking science

19 December 2023

Unless we change it, we’re doomed to the next PLANdemic. And yet, nothing has changed, only got worse! This isn’t pessimism: just a realistic call to ACTION in the medical and scientific freedom communities.

Rethinking education for the real 21st century:

Why not earning $60,000 per year for educating your own children?

Call to action

1. Please share in social networks!

10 shares = waking up more people + especial gratitude:

Waking others up SAVES lives or livelihoods.

For example, send them free ebooks:

Vax-Unvax: Let the Science Speak

The more the awakened, the sooner this nightmare will be over !

2. Please subscribe

Scientific Progress is a reader-supported publication. To receive new posts and support my work, please consider becoming a free or paid subs:

3. Show your love in the tip jar =)

1 dollar makes a difference !

4. Please consider “buy me a coffee”:

5. Please reconsider a paid subscription:

6. Please consider commissioning an article for the topic of your preference:

7. Pray

Most important of all: let’s pray for each other and the conversion of our enemies !

The evil we see in the material world is just the echo from the spiritual battle between God and Satan and their followers, either human or angelic.

Darkness grows because the light of faith is fading. Faith is the root of a plant that withers without the sunlight of love and the water of prayer. God is love: ask Him for more faith in love.

Wow... So much to read, and absorb, and digest... Thank you.

What I'm going to comment on at the moment is in re to the text under "Military" stating that "Air Force [is] offering unused base land for private AI data centers requiring >100 MW each"... I worked for the Bureau of Land Management for years as a Geologist in a field office in Wyoming. I have seen original documentation setting aside areas specifically for "Military Reservations" - yes, that's the terminology. So, not only land patents but also the initial reservation of these lands specifically for military purposes, such as the Executive Orders doing so.

We have gone so far down the road - the opposite direction of the Constitution - of government joining up with private business, that "public-private partnerships" are everywhere, and in virtually every aspect of our lives. It sounds like this BS will / is being used as an excuse for private companies to "use" miliary reservation lands for "military purposes." However, we should all know that that is just an excuse to join military with private corporate interests. And, that that really only serves one master - private corporate interests. Which serves as further evidence that our government and military have been almost completely captured by private corporate interests - and thus, that General Smedley Butler's experience is still occurring, and is fast approaching total consumption / absorption of "our" government and military.

Woe unto us all when that totality occurs. No one will be safe, or secure. We will all be targets. Or, are we there already???